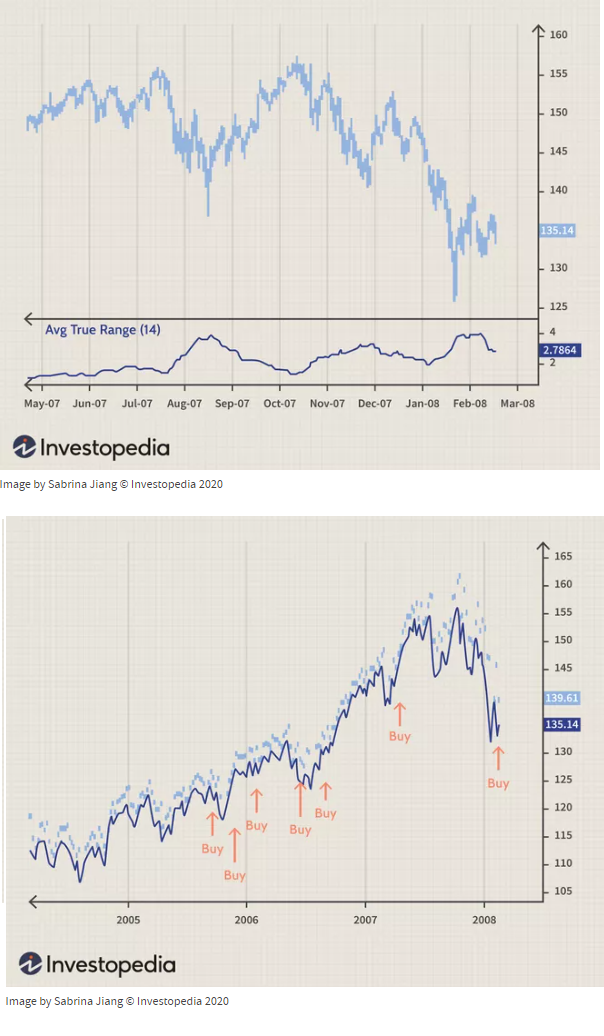

What is Average True Range?

Average True Range is a technical indicator introduced by J. Welles Wilder Jr. in 1978 which measures the volatility or risk of a given stock throughout a 14-day period or longer. The way it is calculated is by using a series of true ranges calculated over a 14-day period. Originally Average True Range was used for tracking the volatility of commodities such as coal or natural gas but in recent times is used in all areas of the modern stock exchange.

The ATR Formula & How To Calculate It

ATR is calculated by taking the sum of the True Ranges calculated over a given period divided by the number of days in the said period.

When calculating ATR there is an order of steps an investor must take, first is to calculate the True Range in one of 3 ways. Firstly, you would take the High on said day and subtract it from the Low on said day. Secondly, you calculate the absolute value (Meaning said value is always positive) of the High on said day subtract the Closing Price on said day. Lastly, you then calculate the absolute value of the Low on said day and subtract the Closing Price on said day.

Now you are to take the highest of these 3 calculations and whichever is the Highest is considered the True Range of the given day. Then once all True Ranges are calculated for the respective amount of days you are to add each day (Take the Sum of) True Range and divide the total by the number of days to get your ATR for the given period.

Things to Note About ATR

There are several things to understand about ATR when calculating as not understanding these facts may lead to misinterpretations when using ATR. Investors should note that using periods shorter than 14 days for ATR can result in more trading indicators than normal. Although, longer periods generate fewer indicators whereas a shorter application around 5 days (Like from Monday to Friday) generates more signals.

What Does the ATR Tell Investors?

Investors should understand that ATR and volatility share a relationship and it goes something like this. Stocks with high ATR indicate higher volatility and higher risk whereas stocks with lower ATR indicate lower volatility and lower risk.

Also, note that ATR is often used to tell an investor when to enter or exit a certain stock however, ATR does not tell an investor the direction of said stocks price but rather only indicates the volatility. As mentioned the ATR is often used as an indicator to exit a stock, one well-known example of this is called the “chandelier exit” which was developed by Chuck LeBeau. Although, besides letting investors know when to exit a stock ATR can also be used to tell investors what size of trade they should be making on derivative stocks.

Limitations of ATR

There are many limitations to using ATR but there are two main ones that should be pointed out. The first thing to note is that ATR is not absolute, meaning that it is subjective to any given investor’s interpretation. Also, note that there is no indefinite ATR value that any investor calculates which tells them exactly when or if a given stock is going trend upwards or downwards. Rather ATR should be used in comparison to prior ATR calculations to get the most accurate depiction of the volatility of a given stock.

Secondly, ATR as mentioned earlier only measures volatility and not if the price of a said stock is going long or short. This can result in inaccurate assumptions on the investor’s part often during pivots in the market. For example, a stock that suddenly shows high volatility after a large gap-up does not necessarily indicate that the stock is volatile etc.

You Might Be Also Interested In:

The 30-year treasury is a US debt security that pays interest every 6 months until they mature, at which point they pay the face amount of the bond

The NASDAQ was created on Feb 8th, 1971, for the purpose of being a safe and secure site where investors could buy & sell securities through a

Market share is a percentile value representing the total sales generated by an individual company in a given industry. One should note that market

For those that do not know what the law of supply and demand is, it is simply the relationship involving the suppliers and consumers of a given